Member content

Already a member? Sign in below

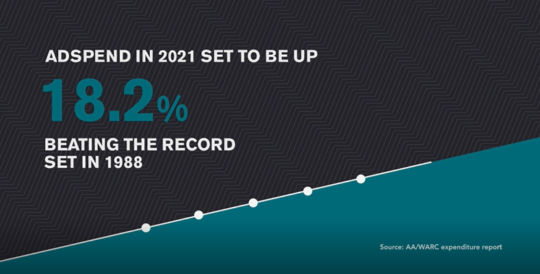

An upgraded forecast of 15.2% growth comes in the latest AA/WARC Expenditure Report published today, which also indicates better-than-expected results for 2020

London, January 26, 2021: The latest Advertising Association/WARC Expenditure Report expects the UK’s ad market to grow by 15.2% this year, an upgrade of 0.8 percentage points from the last forecast in October 2020. The preliminary estimate for growth in 2020 now stands at -7.9% with adspend of £23.17bn – a marked improvement (+6.6 percentage points) since the last outlook, owing mostly to brighter prospects for online platforms.

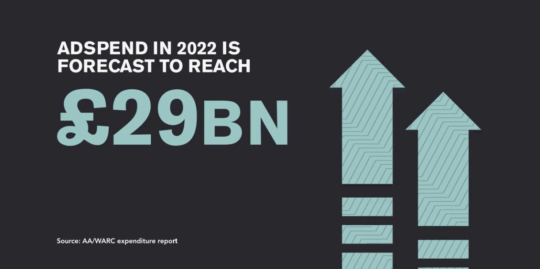

The new forecasts show that the UK’s ad market will make up for 2020’s decline and accelerate further into growth this year, reaching a total of £26.69bn – above the previous high of £25.37bn recorded in 2019. Further, the decline seen in the UK’s ad market during 2020 is estimated to be softer than the global rate (-10.2%) and that of the rest of Europe (-13.7%). The UK’s projected ad market growth in 2021 is also expected to be ahead of key international markets, with the US expected to grow 3.8%, Germany 9.3%, Europe (excluding UK) 8.8%, and China 10.3%.

Internet adspend leads to stronger Q3 2020 performance

The latest dataset includes actual figures for Q3 2020 and predictions for the coming eight quarters. The key findings show that UK adspend fell 3.3% to £5.9bn in Q3 2020. This was far better than the -17.9% forecast in October 2020, owing mostly to better-than-expected internet growth. Internet spend rose 10.1% to £4.2bn during the quarter, buoyed by a 14.5% rise in search spend (which in turn was driven by e-commerce advertising). Overall, UK adspend was down 11.1% over the first nine months of 2020, at £16.2bn.

Fast growth forecast for all media in 2021

Double-digit growth is expected across most media sectors in 2021 – and even triple-figure growth in the case of cinema. Particularly strong results are expected in cinema at 228.4% and reflective of the fact the sector was closed for most of 2020; digital out of home at 53.6%, traditional out of home at 37.7%, and video on demand at 21.2%.

Stephen Woodford, Chief Executive, Advertising Association commented:

“The latest figures from the AA/WARC Expenditure Report come as welcome news at the beginning of the year. Not only does the data show the overall decline expected in 2020 may be less than feared, but the recovery in 2021 will be stronger than we would have dared hope even a few months ago. With the vaccine rollout accelerating and a Brexit trade deal in place, the 2021 business outlook is brightening, reflected by these new forecasts showing a stronger and quicker recovery in adspend, with a stronger rebound than in other large economies. With every £1 of advertising spend generating £6 of GDP, this is good news for jobs and growth in the wider economy.”

James McDonald, Head of Data Content, WARC commented:

“The latest market data show that the largest online properties were shielded from the worst of the industry downturn last year. Indeed, with consumption and commerce migrating online during the pandemic, the results show that ad money followed to these platforms’ benefit.

“Paid search – which accounts for over a third of all advertising spend in the UK – was the format that gained most from a surging e-commerce sector. Ancillary research by WARC shows that online sales recorded a six-year leap in penetration in 2020, as e-commerce’s share of all UK retail value rose by 8.4 percentage points to 27.6%. This rate was ahead of China (24.9%) and double that of the US (13.4%) last year.

“The outlook for the year ahead is bullish, reflecting greater certainty around Brexit and the potential for the vaccination programme to unlock economic growth. We now believe that the ad market can overcorrect in these circumstances to top its 2019 peak, though large parts of the industry remain in a fragile state.”

| Media |

Q3 2020 year-on- year % change |

9M 2020 year-on- year % change |

2020 estimated year-on-year % change |

Percentage point (pp) change in 2020 forecast vs October |

2021 forecast year-on-year % change |

|

Search |

14.5% |

2.5%

|

5.5%

|

+13.0pp |

19.5%

|

|

Online display* |

12.0% |

4.3% |

6.0% |

+9.1pp |

9.3% |

|

TV |

-4.5%

|

-15.1% |

-9.0% |

+3.0pp |

11.6% |

|

of which VOD |

11.9%

|

0.3% |

4.3% |

+2.9pp |

21.2% |

|

Online classified* |

-23.0% |

-29.4% |

-26.0% |

+6.7pp |

16.7% |

|

Direct mail |

-35.9% |

-38.4% |

-35.7% |

-6.0pp |

7.5% |

|

Out of home |

-49.5%

|

-46.5% |

-44.2% |

-4.7pp |

37.7% |

|

of which digital |

-42.1% |

-40.0% |

-38.1% |

-3.1pp |

53.6% |

|

National newsbrands |

-32.3% |

-27.7%

|

-25.7%

|

-0.7pp |

13.8%

|

|

of which online |

-7.9% |

-4.7% |

-3.4% |

+4.1pp |

14.7% |

|

Regional newsbrands |

-39.5% |

-36.0% |

-35.3% |

-2.2pp |

12.3% |

|

of which online |

-29.6% |

-25.8% |

-26.3% |

-1.9pp |

15.4% |

|

Magazine brands |

-38.1% |

-33.6% |

-32.7% |

-4.0pp |

14.6% |

|

of which online |

-28.0% |

-32.3% |

-31.2% |

-4.2pp |

16.1% |

|

Radio |

-5.0% |

-18.6%

|

-15.0%

|

+7.0pp |

12.5%

|

|

of which online |

6.4% |

-11.2%

|

-8.4%

|

+7.5pp |

15.0%

|

|

Cinema |

-96.2%

|

-73.7%

|

-75.8%

|

-11.3pp |

228.4% |

|

TOTAL UK ADSPEND |

-3.3%

|

-11.1%

|

-7.9%

|

+6.6pp |

15.2% |

|

Note: Broadcaster VOD, digital revenues for newsbrands, magazine brands, and radio station websites are also included within online display and classified totals, so care should be taken to avoid double counting. Online radio is display advertising on broadcasters’ websites. |

|||||

|

Forecast year-on-year % change |

Q4 2020 |

Q1 2021 |

Q2 2021 |

Q3 2021 |

Q4 2021 |

Q1 2022 |

|

Search |

14.1% |

10.6% |

42.3% |

17.5% |

15.3% |

9.8% |

|

Online display* |

10.2% |

8.1% |

24.4% |

4.4% |

4.9% |

4.3% |

|

TV |

6.7% |

-0.9% |

55.5% |

9.6% |

1.7% |

4.3% |

|

of which VOD |

14.4% |

10.6% |

58.3% |

14.0% |

17.6% |

11.6% |

|

Online classified* |

-16.0% |

-14.0% |

64.0% |

28.2% |

6.2% |

2.3% |

|

Direct mail |

-28.0% |

-18.0% |

85.0% |

15.0% |

-8.0% |

-8.0% |

|

Out of home |

-38.7% |

-43.5% |

295.7% |

76.8% |

47.8% |

55.3% |

|

of which digital |

-34.1% |

-33.0% |

278.0% |

89.8% |

60.9% |

59.5% |

|

National newsbrands |

-20.7% |

-11.7% |

52.6% |

22.6% |

9.9% |

7.4% |

|

of which online |

-0.4% |

1.5% |

43.5% |

13.6% |

7.4% |

7.7% |

|

Regional newsbrands |

-33.3% |

-21.4% |

52.2% |

22.8% |

16.9% |

7.4%

|

|

of which online |

-28.0% |

-18.7% |

50.8% |

21.2% |

22.1% |

11.1% |

|

Magazine brands |

-30.0% |

-20.5% |

46.5% |

31.8% |

14.3% |

2.0% |

|

of which online |

-28.3% |

-11.3% |

43.2% |

23.3% |

13.4% |

2.9%

|

|

Radio |

-5.0% |

-7.7% |

60.1% |

7.6% |

10.8% |

3.9% |

|

of which online |

-1.0% |

-4.6%

|

54.1% |

5.4% |

17.3% |

12.4%

|

|

Cinema |

-80.0%

|

-76.9%

|

– |

2,227.1%

|

484.8% |

315.1%

|

|

TOTAL UK ADSPEND |

0.4%

|

0.1%

|

46.6% |

15.7%

|

10.3% |

7.6%

|

|

Note: Broadcaster VOD, digital revenues for newsbrands, magazine brands, and radio station websites are also included within online display and classified totals, so care should be taken to avoid double counting. Online radio is display advertising on broadcasters’ websites. |

||||||

|

Market |

2018 year-on-year % change |

2019 year-on-year % change |

2020 estimated year-on-year % change |

2021 forecast year-on-year % change |

|

China |

12.1% |

5.2% |

-3.5% |

10.3% |

|

United States |

10.2% |

4.7% |

-4.1% |

3.8% |

|

Canada |

3.1%

|

6.3% |

-5.6%

|

4.2% |

|

United Kingdom |

8.1% |

7.1%

|

-7.7% |

15.5% |

|

Germany

|

8.9%

|

0.5%

|

-10.6%

|

9.3%

|

|

Europe (excl. UK) |

8.0% |

3.0% |

-13.7% |

8.8% |

|

Global

|

8.0%

|

4.1%

|

-10.2%

|

8.3% |

|

Note: Adspend growth measured in Purchasing Power Parity units. Source: WARC Data |

||||

The Advertising Association/WARC quarterly Expenditure Report is the definitive guide to advertising expenditure in the UK with data and forecasts for different media going back to 1982.

Already a member? Sign in below

If your company is already a member, register your email address now to be able to access our exclusive member-only content.

If your company would like to become a member, please visit our Front Foot page for more details.

Enter your email address to receive a link to reset your password

Your password needs to be at least seven characters. Mixing upper and lower case, numbers and symbols like ! " ? $ % ^ & ) will make it stronger.

If your company is already a member, register your account now to be able to access our exclusive member-only content.